What is the Best Home Loan Tenure: 10, 20, or 30 Years?

In India, home prices have significantly increased, making it difficult to purchase a home outright with cash. As a result, many people are turning to home loans, allowing them to own a home and pay for it comfortably through EMIs.

What is home loan tenure?

Home loan tenure refers to the period within which you must repay your entire home loan through EMIs. For example, you can opt for a tenure of 5, 10, 20, or 30 years.

What is minimum tenure for home loan?

The minimum tenure for a home loan in India is typically as short as 2 years. However, many banks do not offer home loans for such a brief period. For this, the home value needs to be relatively high, so that banks can maximize their profits.

What is the maximum tenure for home loan?

Banks generally offer home loan tenures of up to 30 years. As per RBI guidelines, they cannot offer a tenure longer than 30 years. However, some NBFCs provide home loans with tenures of up to 40 years, though these loans may come with higher interest rates.

How to choose the best home loan tenure?

Choosing the best home loan tenure for yourself involves multiple factors, such as your age, income, and potential future risks. For example, if you are 25 years old, it is easier to get a 30-year home loan. However, if you are over 35, it may be more difficult to secure an extended tenure, unless your income is quite decent.

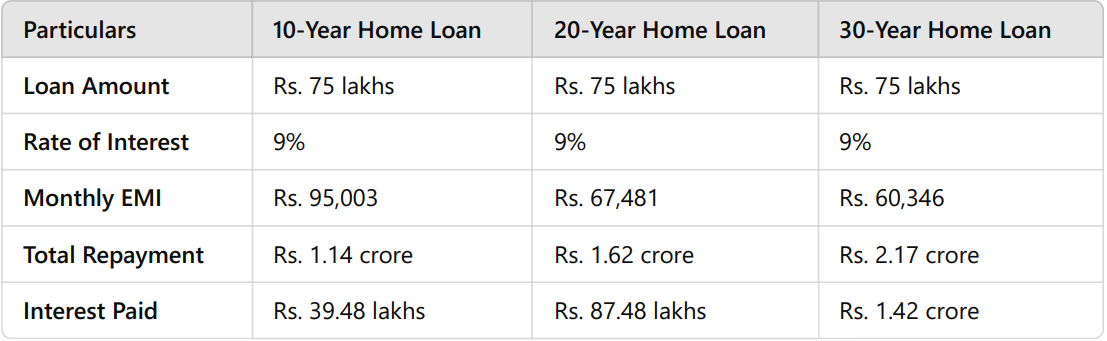

What is the Ideal tenure for home loan?

The table above shows that if you choose a shorter home loan period, the total interest paid will be lower. However, if the tenure increases, the interest will also rise. The benefit of a longer loan is that the monthly EMI will be lower, but the interest rate will be higher.

A general rule for home loans is that your EMI should not exceed 35% of your total salary. With this in mind, choose a tenure that suits your needs, but also consider your age and potential risks.

In my opinion, avoid choosing either a very short or very long loan period. A shorter tenure increases your EMI burden, while a longer tenure increases your interest. Aim for 10, 15, or 20 years for a balanced loan period.

Keep these points in mind when choosing a home loan tenure

• Choose a tenure based on what you can afford.

• EMI should not exceed 35% of your gross salary.

• Shorter tenures lead to higher EMIs but less interest.

• 20-year tenure balances EMI and interest.

• Longer tenures reduce EMI but increase total interest.

• Focus on affordable EMI for better savings.

Foreclosure

If you have a variable-rate home loan, you can foreclose it after the cooling period without any penalty. If you receive a lump sum of money, it's a good idea to use it to pay off the loan, either partially or fully. This will help reduce your debt and bring you closer to fully owning your home.

Remember these things while choosing your home loan tenure

Age factor

If you’re over 45, longer loan tenures may not be an option, so consider shorter ones. If you're under 30, a 20-year tenure is ideal. It allows you to be debt-free by the time you're free, which is a good situation to aim for.

Your income

Affordability is a key issue, and you can manage it in two ways. First, you can check if your income supports the EMI you choose. Second, you can decide based on how much extra you can pay upfront as margin money.

Analyze your investment

If you choose lower EMIs, think about how you will use the money you save. Ask yourself: Will you invest it wisely or spend it on unnecessary things? If you plan for retirement or your child’s education, a longer tenure can be a smart decision.

Property’s value

Check how the value of your property changes in the first five years. If the property value goes up, you might be okay with a longer loan tenure. But if it drops, you might face negative equity, and a shorter tenure would make more sense.

Consider the worst-case scenario. Think about what would happen if you lost your job or business. Can you still afford the EMI? This helps you decide how much EMI you can pay in tough times and choose the right loan tenure.

So, before you opt in for a home loan, never be in hurry. Get your homework done, do your research, read this blog for help and consider all the aspects including current and future. So, you get stress free and don’t feel burdened.

Disclaimer: The information provided in this blog is for general guidance only. Please consult a financial advisor or bank representative for personalized advice on home loans. Interest rates, tenure options, and eligibility may vary based on individual circumstances and lender policies.

.webp)

.webp)

.webp)